CSRD: Be Data Ready

Turn a regulatory obligation into an opportunity to shape your company's sustainable future with data.

The CSRD (Corporate Sustainability Reporting Directive) is a European initiative stemming from the Green Deal.

This new European directive comes into force in 2024. It aims to adjust the prism through which companies approach and communicate their profitability, performance and sustainability.

Indeed, this Directive introduces an obligation of transparency on the three main pillars that enable Corporate Social Responsibility (CSR) to be assessed, with a set of mandatory and standardized publication standards for large companies and listed SMEs.

In brief

- CSRD membership enhances the transparency of sustainability reporting and offers companies a key competitive advantage in the marketplace by highlighting their commitment to sustainability.

- CSRD helps companies to improve data quality and align their sustainability strategy with their long-term objectives.

- Data-driven reporting boosts stakeholder confidence and improves relations with investors.

- Compliance with the CSRD supports the objectives of the European Green Deal and helps to perpetuate sustainable practices.

Turn a regulatory obligation into an opportunity to develop your company's sustainable future thanks to data

The European Green Deal aims to regulate the market through transparency

The main aim of the CSRD is to harmonize companies' sustainability reporting and improve the availability and quality of published ESG data, so that companies in the same sector can be compared.

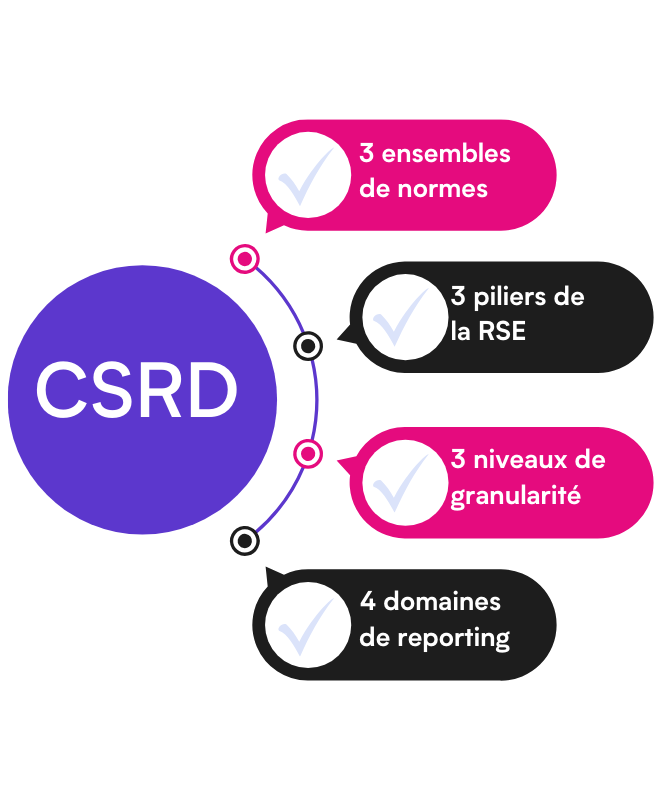

Standards :

- Set 1: All sectors

- Set 2: Sector standards

- Set 3: Entity-specific information (not required but necessary if relevant and material)

Pillars of CSR :

- Environment (E), Social (S), Government (G)

Granularity levels :

- 12 ESRS: 2 transversal, 5 environmental, 4 social and 1 governmental

- 82 Disclosure Requirements (DR)

- 1141 narrative, semi-narrative, digital or hybrid data points

Reporting areas :

- Governance, Strategy and Business Model, Impact, Risk and Opportunity Management, Metrics and Indicators

Non-financial reporting thus becomes sustainability reporting, which, when included in the annual report alongside financial reporting, forms a so-called integrated report. In this way, sustainable performance is placed on the same level as financial performance.

CSRD: changing the rules of the game

The introduction of CSRD represents a change in the rules of the game: the companies that know how to take advantage of it will be those that are able to use it as a lever to identify new competitive advantages.

- CSRD enables companies to identify and mitigate sustainability risks, promoting resilience and long-term value creation.

- It also enhances transparency across the value chain, strengthening trust with stakeholders.

Standardized, reliable ESG data enables investors to assess risks and opportunities more effectively, leading to more informed investment decisions.

By holding companies accountable for their impacts, the CSRD promotes more responsible business practices, contributing to the EU's goals of a sustainable and inclusive economy.

The 10 anticipated long-term benefits of CSRD for businesses

The implementation of the CSRD introduces important changes designed to give sustainable development objectives a more prominent place in corporate strategy, governance and risk management. In addition to its demanding nature, the directive makes it possible to strengthen communication with stakeholders and build a comprehensive vision of the company's challenges.

In this project, Data (especially data availability and quality) and the reporting process are crucial to success.

Micropole's approach to CSRD

Micropole provides its Data, CSR and Analytics experts to produce secure, auditable, high-quality CSRD Reporting.

We can help you bring your operations into line with regulatory requirements specific to your geography, such as CSRD in Europe.

We support you in equipping your organization for sustainability reporting and planning your social and environmental performance.

We audit and support you in defining and achieving your objectives for reducing the environmental footprint of your information systems and IT assets.

The various stages in implementing CSRD

Implementing the CSRD is a transformation project for the company, to at least comply with the Directive and create long-term sustainable value.

Step 1) Inventory and design

Initial diagnosis

- Analysis of the impact of change on the organization: in the context of CSRD, Double Materiality Analysis (DMA) helps to fulfil this role. In fact, the aim of this analysis is to determine the material Sustainability Matters for the company.

- An assessment phase enabling us to draw up an overall assessment of the company's operational mode by analyzing - among other things - strategy, organizational structure and governance, processes, resources and performance management. This analysis takes into account the operational and managerial practices in place to determine the company's level of maturity and define an objective consistent with its ambitions.

Design

Definition of the new operating model: design of the Target Operating Model on the basis of the results of the maturity analysis and the defined objective, and translation into a Data Model.

When the context lends itself to it and if a need is identified, selection of the toolfor which the following macro-steps are identified: formalization of the need, writing of functional and technical specifications, benchmarking of solutions and identification of publishers on the market, launch of a possible call for tenders process, study of technical and financial responses and selection of the tool and of a possible project management (MoE) support for technical integration.

Step 2) Structuring and implementing project management

- This phase consists of progress monitoring, comitology and stakeholder facilitation, and coordination with related projects.

Stage 3) Operational integration

- Integration of the Target Operating Model, as well as tooling when a new tool has to be integrated. This phase includes training for affected employees, implementation of a communication plan and change management actions to ensure the smoothest possible transition.

Step 4) Run

- Operational implementation andcontinuous improvement: we support you through the first iterations of implementation and the launch of a continuous improvement continuous improvement documented of processes.

Step 5) Change management

- Accompanying business employees and partners in this organizational transformation through training and internal and external communication campaigns, where appropriate.

Our assets to support you

A unique ability to support you thanks to recognized expertise across the entire data value chain

Micropole adopts a holistic vision of transformation, supporting you in your Data strategy, organizational, human and technological transformations, from diagnosis to operational implementation.

Our hybrid profile - Consulting / Tech / Digital - responds to this global vision of transformation data driven, to create and manage the entire Data value chain.

Experience in supporting CAC40 companies

Partnerships with market-leading solution providers using advanced technologies

Assets to support change

- Data Thinking

- User experience

Recognized expertise and experience in finance departments

We assist numerous financial departments with their performance management issues via two main pillars:

- Strategy: Finance IS mapping, roadmap building, solution selection assistance, transition management

- Consulting and expertise: project & program management, scoping, design, solution implementation, UAT, change management, user training, operational maintenance

In-depth knowledge of the Directive, enabling us to support you in its operational implementation

Thanks to our partnership with Wequity, we can carry out your CSRD gap analysis in the shortest possible time.

Founded in 2021 by Gabriel Levie and Franck-Victor Laurant, Wequity harnesses the potential of Artificial Intelligence to offer solutions for automated questionnaire processing, ESG data gap analysis and due diligence approaches. Today, Wequity has over 120 customers.

Micropole has signed a partnership agreement with Wequity to operate its CSRD compliance gap analysis solution. Wequity offers an Artificial Intelligence-based solution for automated gap analysis at data point granularity.

In fact, the solution is capable of automatically extracting data and information already available in company documents of heterogeneous natures and formats (internal, external documentation, PDF, XLSX, etc.) and assessing their compliance with the disclosure requirements of CSRD regulations.

This solution, combined with our organizational and data diagnostic tools, simplifies your reporting process and guarantees your compliance with the Directive's requirements.

CSRD in a nutshell

- The CSRD provides a framework for reporting, but in no way imposes an obligation to achieve results.

- It is therefore an obligation to take account of material sustainability issues and to make its strategy part of acontinuous improvement dynamic. Explain uncertainties, possible transition scenarios, ongoing progress, etc.

- The challenge is to measure what is important for the company's transition. In short, don't just try to tick the boxes.

- ESRS should be seen as a tool for steering the transition to a more sustainable economy, rather than a compliance exercise.

- Finally, it's not just a retrospective exercise, it's also, and above all, a forward-looking one.

Ready to start bringing your company into compliance with CSRD regulations?

*This data will be kept for a maximum of three years. In accordance with current regulations, you have the right to oppose, access, rectify, delete and limit your personal data, as well as the right to data portability. These rights may be exercised by contacting privacy@micropole.com. To find out more, consult our privacy policy.

FAQs

Your questions about CSRD

What is CSRD?

The Corporate Sustainability Reporting Directive (CSRD) is a European directive designed to strengthen and extend sustainability reporting obligations for companies. It replaces the Non-Financial Reporting Directive (NFRD) and imposes stricter and more detailed requirements for the publication of information on companies' environmental, social and governance (ESG) impacts.

Who does CSRD concern?

The CSRD is international in scope, as it applies to all major EU companies:

- Companies with more than 250 employees

- Companies with net sales of over 40 million euros

- Companies with total assets in excess of €20 million

- Listed companies, as well as certain listed SMEs, although the latter benefit from more flexible rules

The CSRD also applies to public companies if they meet the size criteria or are listed on an EU stock exchange. These companies must comply with the same reporting requirements as private companies.

What information must be published under the CSRD?

Companies must provide detailed information on the following topics:

- Environmental impacts (CO2 emissions, energy consumption, etc.)

- Social aspects (human rights, working conditions, gender equality)

- Governance (board diversity, anti-corruption policies)

- Sustainability strategies and their integration into the company's business model

These data must be accurate, verifiable and consistent with the ESRS.

When did the CSRD come into force?

The CSRD is being implemented gradually:

- The first companies concerned began reporting in 2024, for fiscal 2023

- For large unlisted companies, the obligation will begin in 2025.

- Listed SMEs will have until 2026 to comply, with the possibility of a derogation until 2028.

What is ESRS (European Sustainability Reporting Standards)?

ESRS are standards developed to guide companies in the preparation of their sustainability reports in accordance with the CSRD. They cover various sustainability-related themes and provide a clear framework for the publication of consistent, comparable and reliable ESG information.

What are the risks of CSRD non-compliance?

Failure to comply with the CSRD may result in :

- Financial penalties

- Damage to reputation

- Difficulties in accessing certain types of financing, as investors and lenders increasingly demand solid ESG reports.

What are the benefits of CSRD compliance?

By complying with the CSRD, a company can :

- Improving transparency and reputation

- Attracting ESG-conscious investors

- Reduce the financial risks associated with sustainability

- Positioning ourselves as leaders in sustainability

What are the international standards recognized by the CSRD?

The CSRD recognizes several international ESG reporting standards, such as the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), the Global Reporting Initiative (GRI) standards, and the Sustainability Accounting Standards Board (SASB) standards.

However, companies must also comply with the European Sustainability Reporting Standards (ESRS).

Does CSRD require an external audit of ESG reports?

Yes, the CSRD requires companies to submit their ESG reports to an external audit. The purpose of this audit is to ensure the reliability of the information published and to strengthen the confidence of investors and other stakeholders.

How does CSRD impact supply chains?

CSRD requires companies to report not only on their own operations, but also on their supply chain. This means they must collect and disclose information on their suppliers' sustainability practices, which may require greater collaboration and transparency along the value chain.

Does CSRD require the inclusion of ESG information in financial reports?

Yes, one of the aims of the CSRD is to integrate ESG information directly into companies' annual management reports, so that this information is considered with the same importance as traditional financial data.